Q3-2025 Property & Casualty market trends

(This overview is provided by our parent company Brown & Brown.)

- Property lines: There’s increased competition in the marketplace for new business, forcing underwriters to consider risks that were previously outside their appetite.

- Property rates are falling in regions prone to natural disasters.

- Workers’ compensation rates continue to be shaped by low-loss activity and carrier competition.

- The umbrella/excess market is challenging, with fewer carriers, reduced limits and increased pricing.

- Nuclear verdicts drive costs and reduce capacity for general/excess liability coverage, creating a renewed focus on tort reform to help mitigate negative impacts.

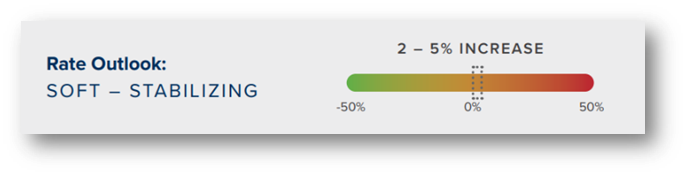

Property Market Trends

After several challenging years in the property insurance market, conditions have become more favorable. Capacity has improved significantly; rates are trending downward, and many carriers are expanding their appetite for new business. This shift can be attributed to the stabilization of supply chains following the pandemic and carriers reaching actuarial rate adequacy.

Higher reported property values are contributing to increased premiums and greater exposure stability, while new entrants in the retail and wholesale sectors are creating more competition. Many underwriters are pursuing ambitious growth goals, further intensifying the race for new business.

Impacts

Through the end of 2025, insureds can anticipate improved pricing, broader terms and enhanced coverage options. Those who faced limitations in capacity or coverage may now find expanded options and more favorable terms.

Carriers remain vigilant regarding valuation accuracy, emphasizing the importance of maintaining up-to-date building values. To help optimize renewal outcomes, valuations can be updated annually and shared with underwriters to improve transparency. Reviewing statements of values and risk management processes may further strengthen underwriting positions.

General Liability Market Trends

For most risks, capacity remains strong, consistent with conditions for the past year. Carriers are seeking new business, thereby creating competition that moderates rate increases. Some areas still face challenges, such as construction, residential/habitational and large retail strip centers. Additionally, there is limited access to coverage for assault and battery risks associated with real estate or large retail and restaurant exposures.

Impacts

Small and middle market accounts can anticipate rates ranging from flat to +10%. Accounts experiencing loss activity may face limited market availability, with new restrictive exclusions. To adapt to the market, organizations can consider focusing on risk management. Real estate accounts should implement strong controls over the properties they own or manage to help mitigate hazards. A strong security posture is also preferred.

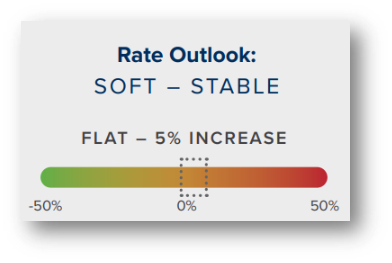

Workers’ Compensation Market Trends

The workers’ compensation space remains a soft and stable market. Depending on loss activity and experience modifications, renewal rates range from flat to 5%. For low-loss accounts, rates could decrease by 5-15%, not including experience modification changes.

from flat to 5%. For low-loss accounts, rates could decrease by 5-15%, not including experience modification changes.

Impacts

Carriers are focused on pre-quote loss control to qualify accounts. Insureds can adapt by focusing on risk management practices and loss control. When considering best practices for risk management, a great place to start is talent acquisition and safety programs.

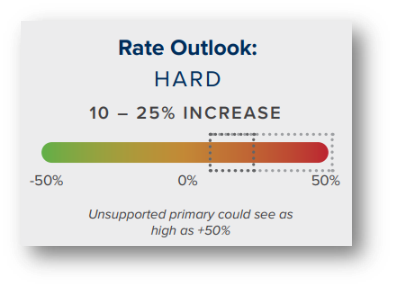

Umbrella/Excess Market Trends

Umbrella/excess renewals face a challenging marketplace. The space seeks rate adequacy as it faces nuclear verdicts, which impact their reserve adequacy. Supported umbrellas, where the same carrier writes the underlying and lead umbrella, face reduced capacity. For higher-risk industries, limits may be halved and paired with higher premiums.

adequacy. Supported umbrellas, where the same carrier writes the underlying and lead umbrella, face reduced capacity. For higher-risk industries, limits may be halved and paired with higher premiums.

Unsupported umbrellas/excess are more challenging, with a shrinking number of markets providing capacity, while remaining markets can deploy their capacity based on restrictive underwriting and price escalations.

Unilateral underwriter decision-making across portfolios will impact all renewals. MGAs are reintroducing shared risk purchasing groups to provide limits and pricing options on a limited basis.

Impacts

Accounts with a supported umbrella coverage may experience a hard to stable market. An unsupported umbrella remains hard and is becoming more challenging.

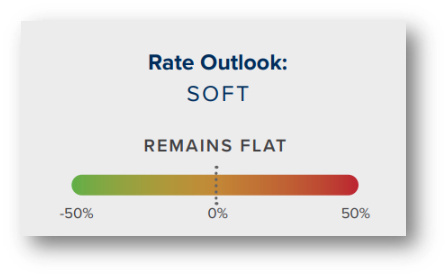

Cyber Risk Market Trends

Due to increased premium volume and decreased losses, competition characterizes the cyber arena. Decreased claims severity, combined with improved underwriting and security controls, help to drive down premiums.

Underwriters remain concerned about privacy regulation claims, with some carriers opting to limit coverage for unlawful collection. Additionally, underwriters continue to evaluate critical cyber and privacy controls, including those listed below. Your customers should consider other controls for more favorable offerings.

- Multi-factor authentication (MFA)

- Endpoint detection response (EDR)

- Backup procedures

- Employee training

- Incident response

- Business continuity plans

- Annual testing

Recent events carried out by the highly disruptive cybercrime group Scattered Spider highlight the importance of strengthening defenses at the human level. The group’s industry-focused campaign tactics rely heavily on social engineering. The market is aware of multiple intrusions in the insurance industry that bear the hallmarks of Scattered Spider activity. Help your companies focus on employee training, strict identity verification and access monitoring to protect against this evolving threat is strongly encouraged.

Impacts

Current market conditions are favorable for insureds, with renewal rates remaining flat and the potential for decreased rates for excess layers. After several years of carriers hesitating to broaden their products to compete, they have become more willing to offer broader terms. Carriers more frequently deploy increased capacity with competitive retentions, particularly for buyers with good controls. Many buyers are taking advantage of this market cycle, buying more limits and expanding coverage.